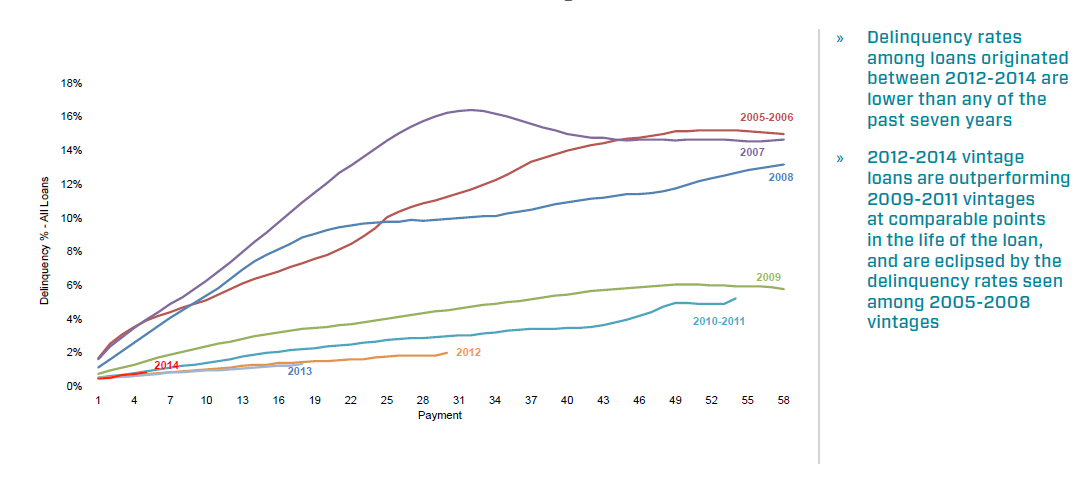

David Dayen of the liberal New Republic recently reported on a speech by Mel Watts, the chairman of the Federal Housing Finance Agency (FHFA), which has served as the conservator for Fannie Mae and Freddie Mac since the financial crisis. Dayen argues that Watt “signaled to mortgage bankers that they can loosen their underwriting standards, and that Fannie and Freddie will purchase the loans anyway, without much recourse if they turn sour.” While the reasons for the financial crisis are many, it cannot be argued that loose lending did not play a major role. Well, on January 10, 2014, the Consumer Financial Protection Bureau’s Ability-To-Repay Rule went into effect, which has caused some tightening in the lending world.

Dayen, in much more pointed terms argues that:

the mortgage industry has engaged in an insidious tactic: tightening lending well beyond required standards, and then claiming the GSEs make it impossible for them to do business. For example, Fannie and Freddie require a minimum 680 credit score to purchase most loans, but lenders are setting their targets at 740. They are rejecting eligible borrowers (which, after all, make lenders money) so they can profit much more from a regulation-free zone down the line.

Let’s call this what it is: a shakedown. You can see this clearly from the opening session of the Mortgage Bankers Association conference, where the trade group’s leadership sounded more like mob dons. “If they’re going to regulate us, they must work to better understand the unintended consequences on consumers,” said MBA Chairman Bill Cosgrove. “Enforcement should be the exception to the rule, not the rule itself,” added President David Stevens. Concluded Cosgrove, “Today’s lenders are paying many times over for mistakes that may have been out of their control… It’s time for the penalty phase to end.” Nice mortgage market you’ve got there; shame if something happened to it.

Sadly, Watt, the FHFA chairman, has paid attention to these howls of protest, and has scrambled to “open the credit box,” to use the industry term. In Monday’s speech, he announced additional changes to the representations and warranties language. Generally speaking, the GSEs limit buybacks to the first three years. But they can demand buybacks later in certain prescribed cases of fraud, data inaccuracies or misrepresentation. However, Watt announced that his agency would establish “a minimum number of loans that must be identified with misrepresentations or data inaccuracies” to trigger the buybacks. In other words, lenders can now pass the GSEs a certain number of fraudulent loans, as long as they stay below the threshold.

He concludes with this thought:

Fixing the housing market requires putting people in the financial position to carry a mortgage, not slashing lending standards. It’s as if government’s best and brightest threw up their hands, deciding they had to return to bubble economics as the only way to produce growth. This has the lending industry, which profits handsomely from bubbles on the way up, licking their chops, especially if they can sell off the loans to the taxpayer and let them deal with the consequences. Given what we know about how lenders shuttled borrowers with weak credit into loans they couldn’t afford, the prospect of a rerun should be frightening enough for any policymaker to reject. But the industry played Mel Watt and other officials like a fiddle, and we’ll all be singing the blues in the aftermath.

I leave it to the reader to decide if they agree with Dayen’s conclusion, but for all the books I was reading during the financial crisis detailing the tactics of the likes of New Century, Ameriquest, Countrywide, and the major banks, it is hard to argue with some tightening in the lending world. Yes, it will keep some people out of the housing market, but maybe that is exactly how it should have been in the first place. Maybe we should learn from Ed Clark, a plainspoken, polite and prudent Canadian bank CEO with a few simple rules: “We should never do things for our customers and clients that we don’t actually understand. If you wouldn’t put your mother-in-law in this, don’t put our clients in it.” Simple advice – just not followed south of the Canadian border.